Find change points efficiently in exponentially distributed data

Source:R/fastcpd.R

fastcpd_exponential.Rdfastcpd_exponential() and fastcpd.exponential() are

wrapper functions of fastcpd() to find changes in the rate of

exponentially distributed data, i.e. mean change under exponentially

distributed noise (cf. changepoint::cpt.meanvar with

test.stat = "Exponential"). The function is similar to

fastcpd() except that the data is by default a matrix or data frame or

a vector with each row / element as an observation and thus a formula is

not required here.

Arguments

- data

A matrix, a data frame or a vector.

- ...

Other arguments passed to

fastcpd(), for example,segment_count.

Value

A fastcpd object.

Examples

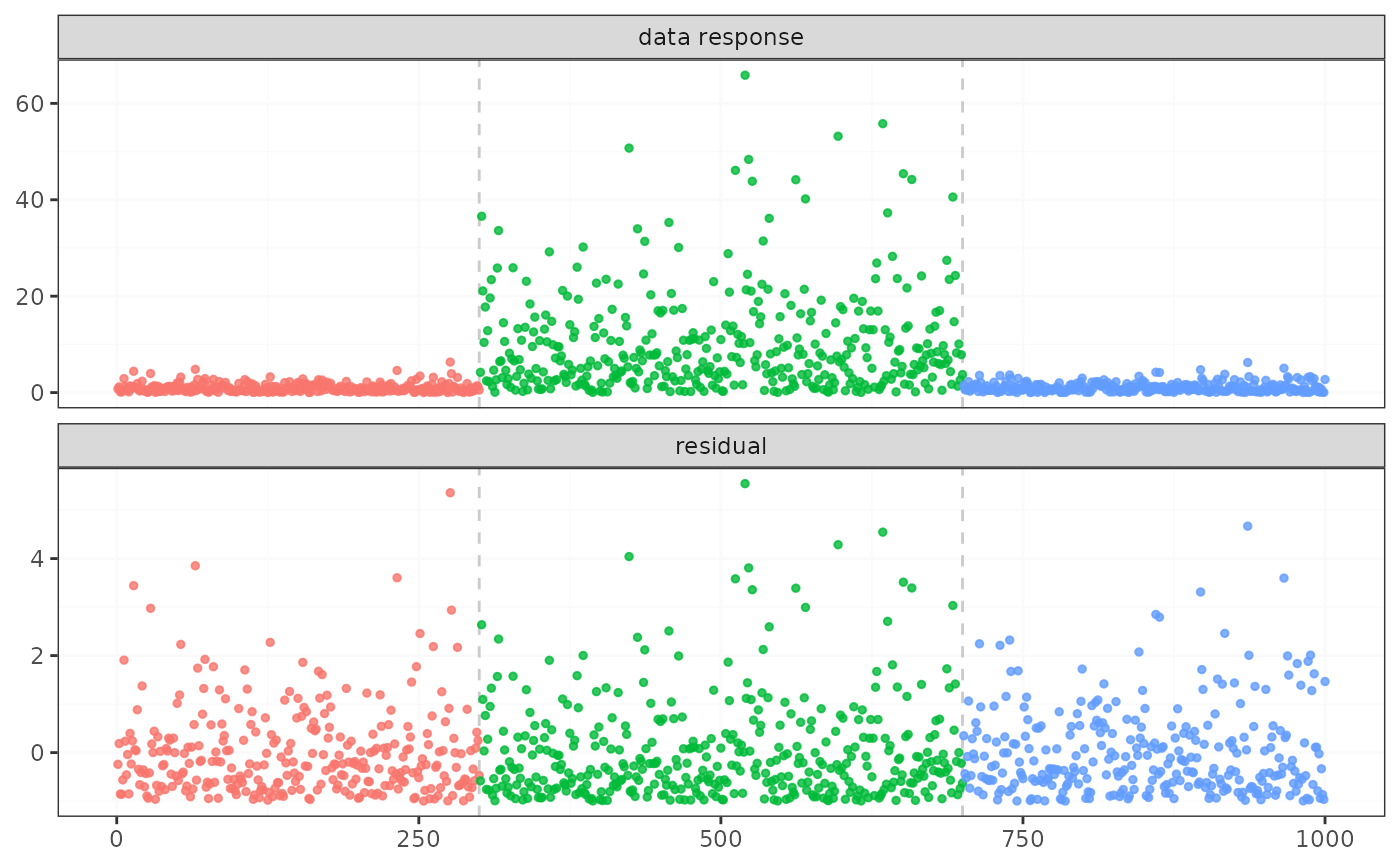

set.seed(1)

data <- matrix(c(

rexp(300, rate = 1),

rexp(400, rate = 0.1),

rexp(300, rate = 1)

))

system.time(result <- fastcpd.exponential(data))

#> user system elapsed

#> 0.002 0.000 0.002

summary(result)

#>

#> Call:

#> fastcpd.exponential(data = data)

#>

#> Change points:

#> 300 700

#>

#> Cost values:

#> 301.6378 1326.448 331.5256

#>

#> Parameters:

#> segment 1 segment 2 segment 3

#> 1 1.004055 0.09939726 0.9088465

plot(result)