fastcpd_garch() and fastcpd.garch() are

wrapper functions of fastcpd() to find change points in

GARCH(\(p\), \(q\)) models. The function is similar to fastcpd()

except that the data is by default a one-column matrix or univariate vector

and thus a formula is not required here.

Arguments

- data

A numeric vector, a matrix, a data frame or a time series object.

- order

A positive integer vector of length two specifying the order of the GARCH model.

- ...

Other arguments passed to

fastcpd(), for example,segment_count.

Value

A fastcpd object.

Examples

# \donttest{

set.seed(1)

n <- 401

sigma_2 <- rep(1, n + 1)

x <- rep(0, n + 1)

for (i in seq_len(200)) {

sigma_2[i + 1] <- 20 + 0.8 * x[i]^2 + 0.1 * sigma_2[i]

x[i + 1] <- rnorm(1, 0, sqrt(sigma_2[i + 1]))

}

for (i in 201:n) {

sigma_2[i + 1] <- 1 + 0.1 * x[i]^2 + 0.5 * sigma_2[i]

x[i + 1] <- rnorm(1, 0, sqrt(sigma_2[i + 1]))

}

result <- suppressWarnings(

fastcpd.garch(x[-1], c(1, 1), include.mean = FALSE)

)

summary(result)

#>

#> Call:

#> fastcpd.garch(data = x[-1], order = c(1, 1), include.mean = FALSE)

#>

#> Change points:

#> 205

#>

#> Cost values:

#> 491.9506 188.9431

#>

#> Parameters:

#> segment 1 segment 2

#> 1 11.5363695 1.9983858

#> 2 0.4695383 0.0128258

#> 3 0.3428052 0.1368199

plot(result)

# }

# \donttest{

set.seed(1)

n <- 120

sigma_2 <- rep(1, n + 1)

x <- rep(0, n + 1)

for (i in seq_len(60)) {

sigma_2[i + 1] <- 10 + 0.5 * x[i]^2 + 0.3 * sigma_2[i]

x[i + 1] <- rnorm(1, 0, sqrt(sigma_2[i + 1]))

}

for (i in 61:n) {

sigma_2[i + 1] <- 0.2 + 0.05 * x[i]^2 + 0.1 * sigma_2[i]

x[i + 1] <- rnorm(1, 0, sqrt(sigma_2[i + 1]))

}

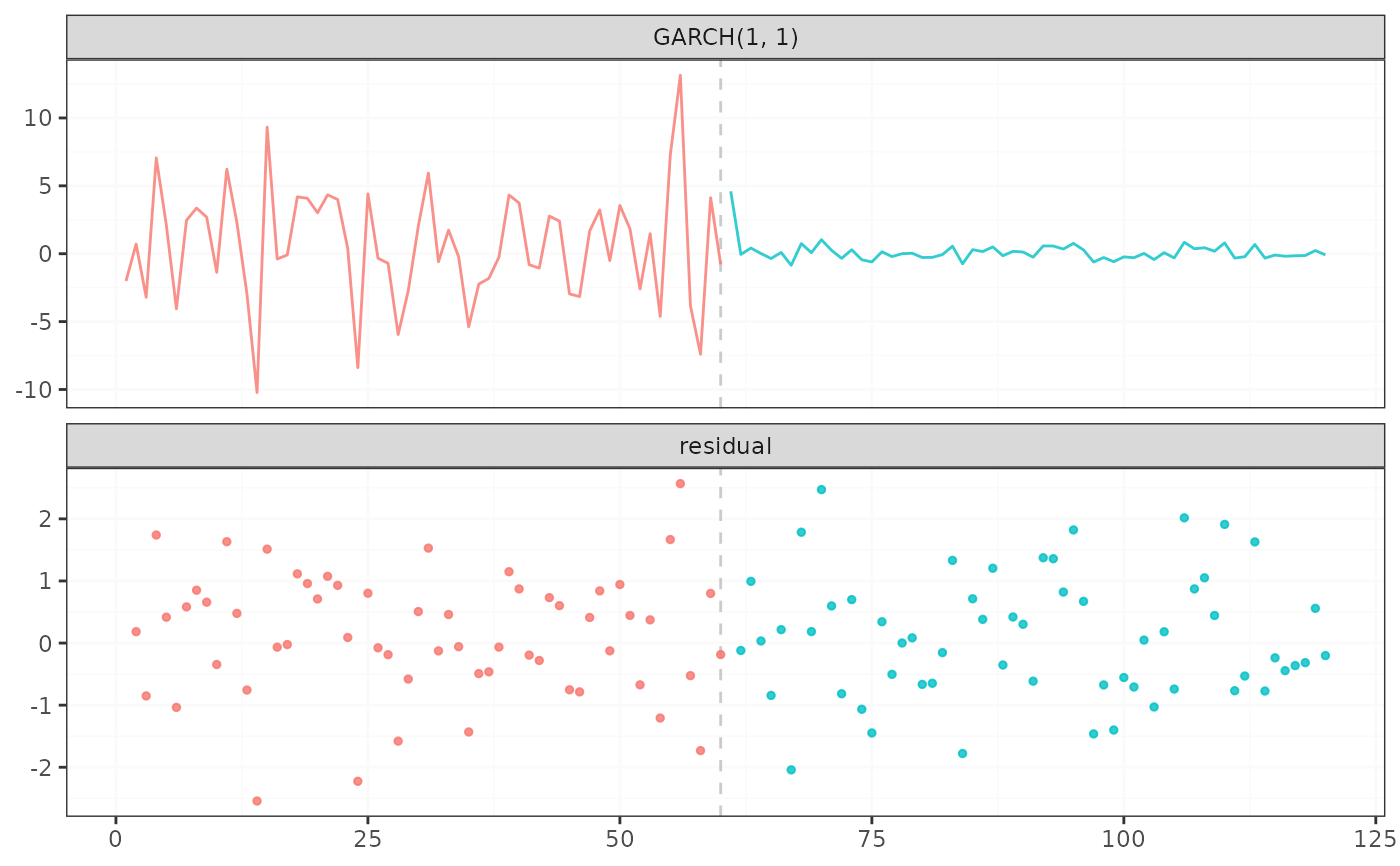

result <- suppressWarnings(

fastcpd.garch(x[-1], c(1, 1), include.mean = FALSE)

)

summary(result)

#>

#> Call:

#> fastcpd.garch(data = x[-1], order = c(1, 1), include.mean = FALSE)

#>

#> Change points:

#> 60

#>

#> Cost values:

#> 120.2821 -15.87097

#>

#> Parameters:

#> segment 1 segment 2

#> 1 13.8346334 0.174438

#> 2 0.2278886 0.000000

#> 3 0.0200848 0.000000

plot(result)

# }

# \donttest{

set.seed(1)

n <- 120

sigma_2 <- rep(1, n + 1)

x <- rep(0, n + 1)

for (i in seq_len(60)) {

sigma_2[i + 1] <- 10 + 0.5 * x[i]^2 + 0.3 * sigma_2[i]

x[i + 1] <- rnorm(1, 0, sqrt(sigma_2[i + 1]))

}

for (i in 61:n) {

sigma_2[i + 1] <- 0.2 + 0.05 * x[i]^2 + 0.1 * sigma_2[i]

x[i + 1] <- rnorm(1, 0, sqrt(sigma_2[i + 1]))

}

result <- suppressWarnings(

fastcpd.garch(x[-1], c(1, 1), include.mean = FALSE)

)

summary(result)

#>

#> Call:

#> fastcpd.garch(data = x[-1], order = c(1, 1), include.mean = FALSE)

#>

#> Change points:

#> 60

#>

#> Cost values:

#> 120.2821 -15.87097

#>

#> Parameters:

#> segment 1 segment 2

#> 1 13.8346334 0.174438

#> 2 0.2278886 0.000000

#> 3 0.0200848 0.000000

plot(result)

# }

# \donttest{

set.seed(1)

n <- 150

sigma_2 <- rep(1, n + 1)

x <- rep(0, n + 1)

for (i in seq_len(75)) {

sigma_2[i + 1] <- 10 + 0.5 * x[i]^2 + 0.3 * sigma_2[i]

x[i + 1] <- rnorm(1, 0, sqrt(sigma_2[i + 1]))

}

for (i in 76:n) {

sigma_2[i + 1] <- 0.2 + 0.05 * x[i]^2 + 0.1 * sigma_2[i]

x[i + 1] <- rnorm(1, 0, sqrt(sigma_2[i + 1]))

}

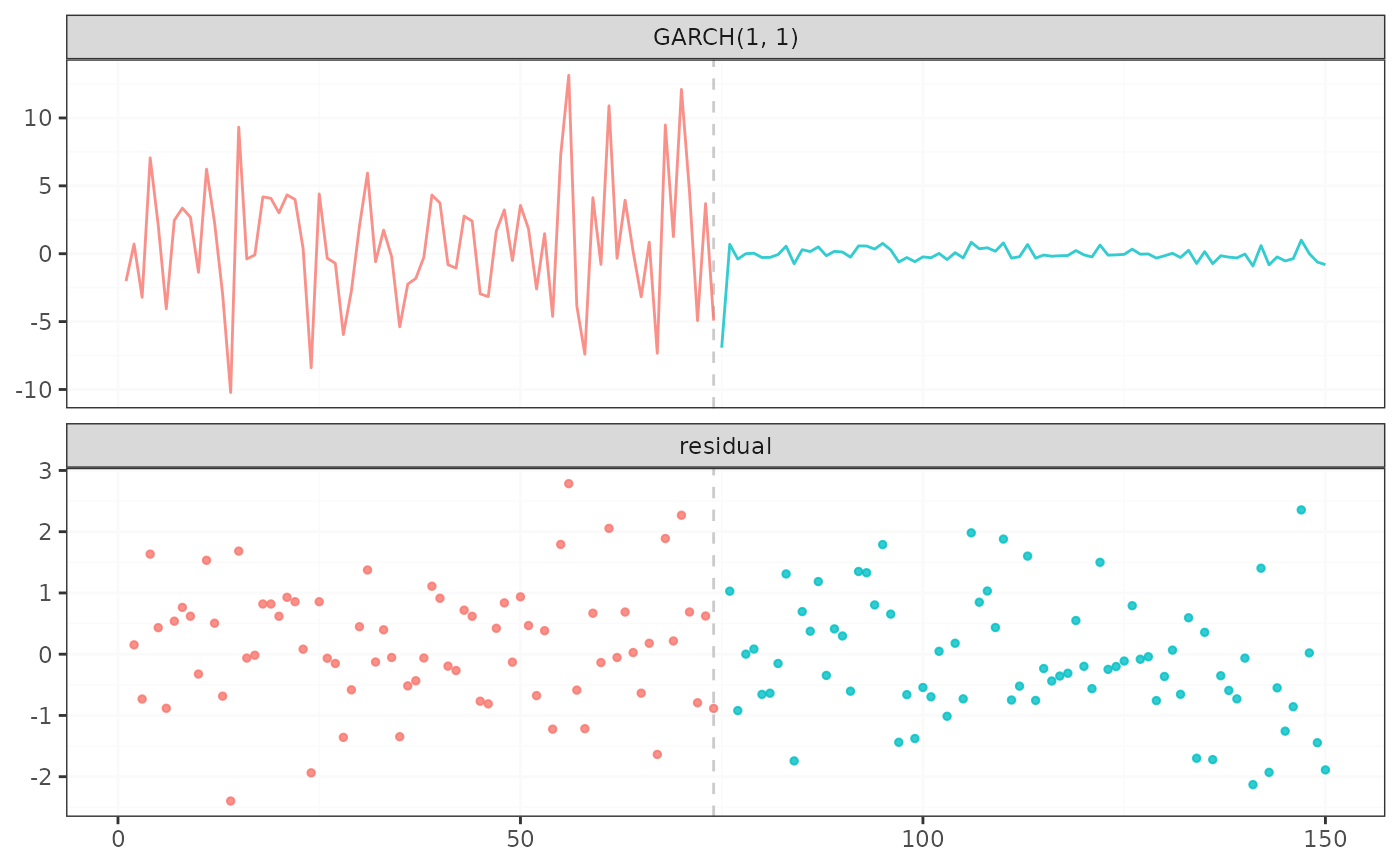

result <- suppressWarnings(

fastcpd.garch(x[-1], c(1, 1), include.mean = FALSE)

)

summary(result)

#>

#> Call:

#> fastcpd.garch(data = x[-1], order = c(1, 1), include.mean = FALSE)

#>

#> Change points:

#> 74

#>

#> Cost values:

#> 154.8803 -19.62733

#>

#> Parameters:

#> segment 1 segment 2

#> 1 2.8412668 0.180061756

#> 2 0.1358175 0.005695202

#> 3 0.7489304 0.000000000

plot(result)

# }

# \donttest{

set.seed(1)

n <- 150

sigma_2 <- rep(1, n + 1)

x <- rep(0, n + 1)

for (i in seq_len(75)) {

sigma_2[i + 1] <- 10 + 0.5 * x[i]^2 + 0.3 * sigma_2[i]

x[i + 1] <- rnorm(1, 0, sqrt(sigma_2[i + 1]))

}

for (i in 76:n) {

sigma_2[i + 1] <- 0.2 + 0.05 * x[i]^2 + 0.1 * sigma_2[i]

x[i + 1] <- rnorm(1, 0, sqrt(sigma_2[i + 1]))

}

result <- suppressWarnings(

fastcpd.garch(x[-1], c(1, 1), include.mean = FALSE)

)

summary(result)

#>

#> Call:

#> fastcpd.garch(data = x[-1], order = c(1, 1), include.mean = FALSE)

#>

#> Change points:

#> 74

#>

#> Cost values:

#> 154.8803 -19.62733

#>

#> Parameters:

#> segment 1 segment 2

#> 1 2.8412668 0.180061756

#> 2 0.1358175 0.005695202

#> 3 0.7489304 0.000000000

plot(result)

# }

# }