fastcpd_lm() and fastcpd.lm() are wrapper

functions of fastcpd() to find change points in linear

regression models. The function is similar to fastcpd() except that

the data is by default a matrix or data frame with the response variable

as the first column and thus a formula is not required here.

Arguments

- data

A matrix or a data frame with the response variable as the first column.

- ...

Other arguments passed to

fastcpd(), for example,segment_count.

Value

A fastcpd object.

Examples

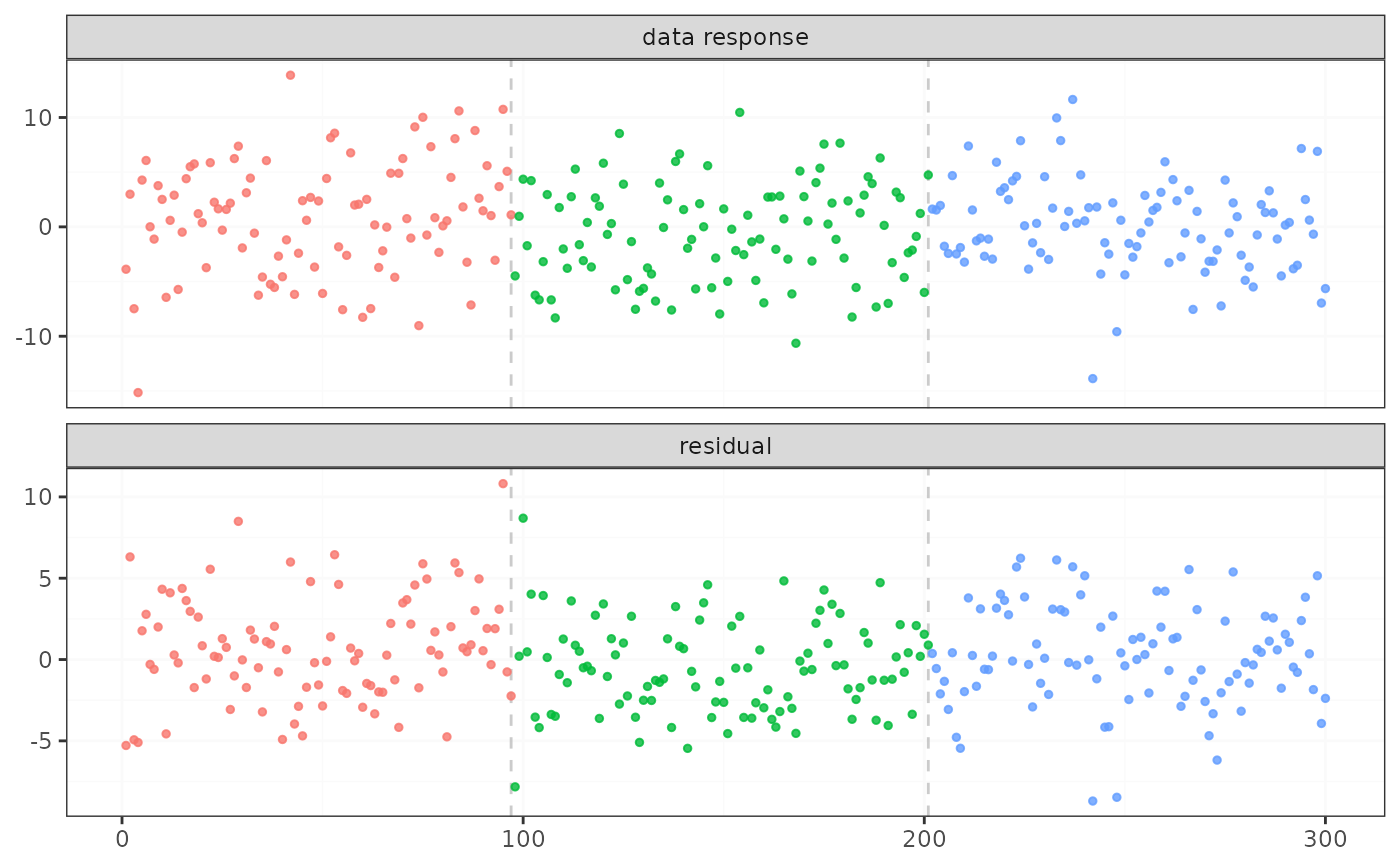

if (requireNamespace("mvtnorm", quietly = TRUE)) {

set.seed(1)

n <- 300

p <- 4

x <- mvtnorm::rmvnorm(n, rep(0, p), diag(p))

theta_0 <- rbind(c(1, 3.2, -1, 0), c(-1, -0.5, 2.5, -2), c(0.8, 0, 1, 2))

y <- c(

x[1:100, ] %*% theta_0[1, ] + rnorm(100, 0, 3),

x[101:200, ] %*% theta_0[2, ] + rnorm(100, 0, 3),

x[201:n, ] %*% theta_0[3, ] + rnorm(100, 0, 3)

)

result_lm <- fastcpd.lm(cbind(y, x))

summary(result_lm)

plot(result_lm)

}

#>

#> Call:

#> fastcpd.lm(data = cbind(y, x))

#>

#> Change points:

#> 97 201

#>

#> Cost values:

#> 528.9771 424.3702 471.2645

#>

#> Parameters:

#> segment 1 segment 2 segment 3

#> 1 0.74291290 -0.6153049 0.8733473

#> 2 3.69465275 -0.5034948 0.3222868

#> 3 -1.24746871 2.2522352 1.0188455

#> 4 0.09579985 -1.9875126 2.2761340

# \donttest{

if (requireNamespace("mvtnorm", quietly = TRUE)) {

set.seed(1)

n <- 600

p <- 4

d <- 2

x <- mvtnorm::rmvnorm(n, rep(0, p), diag(p))

theta_1 <- matrix(runif(8, -3, -1), nrow = p)

theta_2 <- matrix(runif(8, -1, 3), nrow = p)

y <- rbind(

x[1:350, ] %*% theta_1 + mvtnorm::rmvnorm(350, rep(0, d), 3 * diag(d)),

x[351:n, ] %*% theta_2 + mvtnorm::rmvnorm(250, rep(0, d), 3 * diag(d))

)

result_mlm <- fastcpd.lm(cbind.data.frame(y = y, x = x), p.response = 2)

summary(result_mlm)

}

#>

#> Call:

#> fastcpd.lm(data = cbind.data.frame(y = y, x = x), p.response = 2)

#>

#> Change points:

#> 350

#>

#> Cost values:

#> 1431.421 1019.442

#>

#> Parameters:

#> segment 1 segment 2

#> 1 -2.453012 1.68044714

#> 2 -2.295667 -0.46458087

#> 3 -1.327543 1.07765071

#> 4 -2.783358 -0.15196831

#> 5 -1.895117 2.86434615

#> 6 -1.927478 2.61647011

#> 7 -1.168885 1.73783271

#> 8 -1.380168 0.09453771

# }

# \donttest{

if (requireNamespace("mvtnorm", quietly = TRUE)) {

set.seed(1)

n <- 600

p <- 4

d <- 2

x <- mvtnorm::rmvnorm(n, rep(0, p), diag(p))

theta_1 <- matrix(runif(8, -3, -1), nrow = p)

theta_2 <- matrix(runif(8, -1, 3), nrow = p)

y <- rbind(

x[1:350, ] %*% theta_1 + mvtnorm::rmvnorm(350, rep(0, d), 3 * diag(d)),

x[351:n, ] %*% theta_2 + mvtnorm::rmvnorm(250, rep(0, d), 3 * diag(d))

)

result_mlm <- fastcpd.lm(cbind.data.frame(y = y, x = x), p.response = 2)

summary(result_mlm)

}

#>

#> Call:

#> fastcpd.lm(data = cbind.data.frame(y = y, x = x), p.response = 2)

#>

#> Change points:

#> 350

#>

#> Cost values:

#> 1431.421 1019.442

#>

#> Parameters:

#> segment 1 segment 2

#> 1 -2.453012 1.68044714

#> 2 -2.295667 -0.46458087

#> 3 -1.327543 1.07765071

#> 4 -2.783358 -0.15196831

#> 5 -1.895117 2.86434615

#> 6 -1.927478 2.61647011

#> 7 -1.168885 1.73783271

#> 8 -1.380168 0.09453771

# }