fastcpd_ts() and fastcpd.ts() are wrapper functions for

fastcpd() to find change points in time series data. The function is

similar to fastcpd() except that the data is a time series and the

family is one of "ar", "var", "arma", "arima" or

"garch".

Arguments

- data

A numeric vector, a matrix, a data frame or a time series object.

- family

A character string specifying the family of the time series. The value should be one of

"ar","var","arima"or"garch".- order

A positive integer or a vector of length less than four specifying the order of the time series. Possible combinations with

familyare:"ar", NUMERIC(1): AR(\(p\)) model using linear regression."var", NUMERIC(1): VAR(\(p\)) model using linear regression."arima", NUMERIC(3): ARIMA(\(p\), \(d\), \(q\)) model usingstats::arima()."garch", NUMERIC(2): GARCH(\(p\), \(q\)) model.

- ...

Other arguments passed to

fastcpd(), for example,segment_count. One special argument can be passed here isinclude.mean, which is a logical value indicating whether the mean should be included in the model. The default value isTRUE.

Value

A fastcpd object.

Examples

# \donttest{

# Set seed for reproducibility

set.seed(1)

# 1. Define Parameters

n <- 500 # Total length of the time series

cp1 <- 200 # First change point at time 200

cp2 <- 350 # Second change point at time 350

# Define MA(2) coefficients for each segment ensuring invertibility

# MA coefficients affect invertibility; to ensure invertibility, the roots of

# the MA polynomial should lie outside the unit circle.

# Segment 1: Time 1 to cp1

theta1_1 <- 0.5

theta2_1 <- -0.3

# Segment 2: Time (cp1+1) to cp2

theta1_2 <- -0.4

theta2_2 <- 0.25

# Segment 3: Time (cp2+1) to n

theta1_3 <- 0.6

theta2_3 <- -0.35

# Function to check invertibility for MA(2)

is_invertible_ma2 <- function(theta1, theta2) {

# The MA(2) polynomial is: 1 + theta1*z + theta2*z^2 = 0

# Compute the roots of the polynomial

roots <- polyroot(c(1, theta1, theta2))

# Invertible if all roots lie outside the unit circle

all(Mod(roots) > 1)

}

# Verify invertibility for each segment

stopifnot(is_invertible_ma2(theta1_1, theta2_1))

stopifnot(is_invertible_ma2(theta1_2, theta2_2))

stopifnot(is_invertible_ma2(theta1_3, theta2_3))

# 2. Simulate White Noise

e <- rnorm(n + 2, mean = 0, sd = 1) # Extra terms to handle lag

# 3. Initialize the Time Series

y <- numeric(n + 2) # Extra terms for initial lags (y[1], y[2] are zero)

# 4. Apply MA(2) Model with Change Points

for (t in 3:(n + 2)) { # Start from 3 to have enough lags for MA(2)

# Determine current segment

current_time <- t - 2 # Adjust for the extra lags

if (current_time <= cp1) {

theta <- c(theta1_1, theta2_1)

} else if (current_time <= cp2) {

theta <- c(theta1_2, theta2_2)

} else {

theta <- c(theta1_3, theta2_3)

}

# Compute MA(2) value

y[t] <- e[t] + theta[1] * e[t - 1] + theta[2] * e[t - 2]

}

# Remove the initial extra terms

y <- y[3:(n + 2)]

time <- 1:n

# Function to get roots data for plotting

get_roots_data <- function(theta1, theta2, segment) {

roots <- polyroot(c(1, theta1, theta2))

data.frame(

Re = Re(roots),

Im = Im(roots),

Distance = Mod(roots),

Segment = segment

)

}

roots_segment1 <- get_roots_data(theta1_1, theta2_1, "Segment 1")

roots_segment2 <- get_roots_data(theta1_2, theta2_2, "Segment 2")

roots_segment3 <- get_roots_data(theta1_3, theta2_3, "Segment 3")

(roots_data <- rbind(roots_segment1, roots_segment2, roots_segment3))

#> Re Im Distance Segment

#> 1 -1.173599 -5.752739e-16 1.173599 Segment 1

#> 2 2.840266 5.752739e-16 2.840266 Segment 1

#> 3 0.800000 1.833030e+00 2.000000 Segment 2

#> 4 0.800000 -1.833030e+00 2.000000 Segment 2

#> 5 -1.038071 -1.180701e-18 1.038071 Segment 3

#> 6 2.752357 1.180701e-18 2.752357 Segment 3

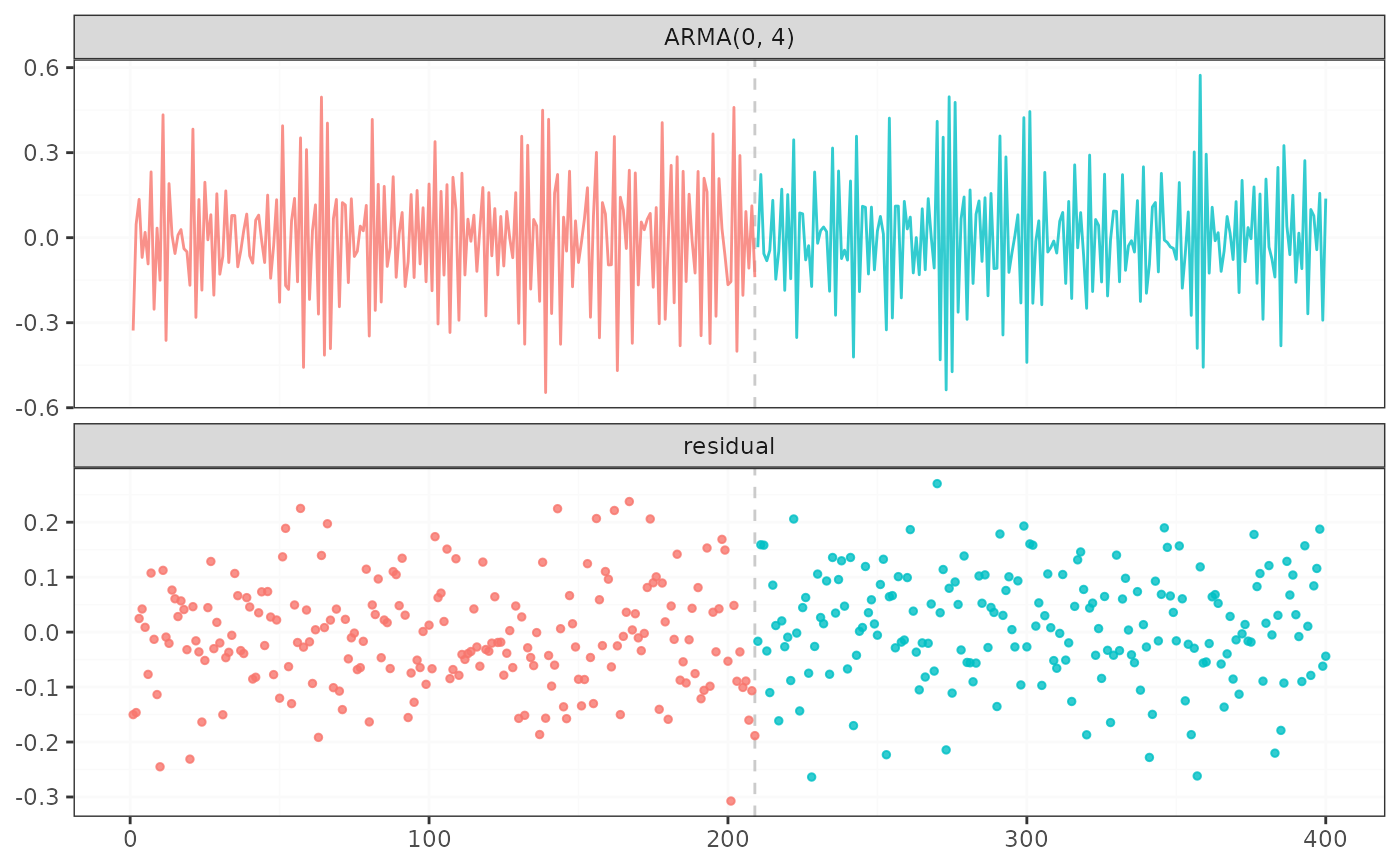

result <- fastcpd.ts(

y,

"arma",

c(0, 2),

lower = c(-2, -2, 1e-10),

upper = c(2, 2, Inf),

line_search = c(1, 0.1, 1e-2),

trim = 0.04

)

summary(result)

#>

#> Call:

#> fastcpd.ts(data = y, family = "arma", order = c(0, 2), lower = c(-2,

#> -2, 1e-10), upper = c(2, 2, Inf), line_search = c(1, 0.1,

#> 0.01), trim = 0.04)

#>

#> Change points:

#> 203 356

#>

#> Cost values:

#> 281.9365 227.2833 225.577

#>

#> Parameters:

#> segment 1 segment 2 segment 3

#> 1 0.5078778 -0.4503257 0.6216567

#> 2 -0.3659674 0.2392667 -0.3661703

#> 3 0.8648758 1.0333588 1.1822668

plot(result)

# }

# }